Car

How to Finance a Car: Practical Tips to Close the Best Deal!

Thinking about buying a car but don't have the full amount? Discover how to finance a car simply, without complications, and make your dream come true faster!

Advertisement

Discover the best strategies to finance your car safely and without complications!

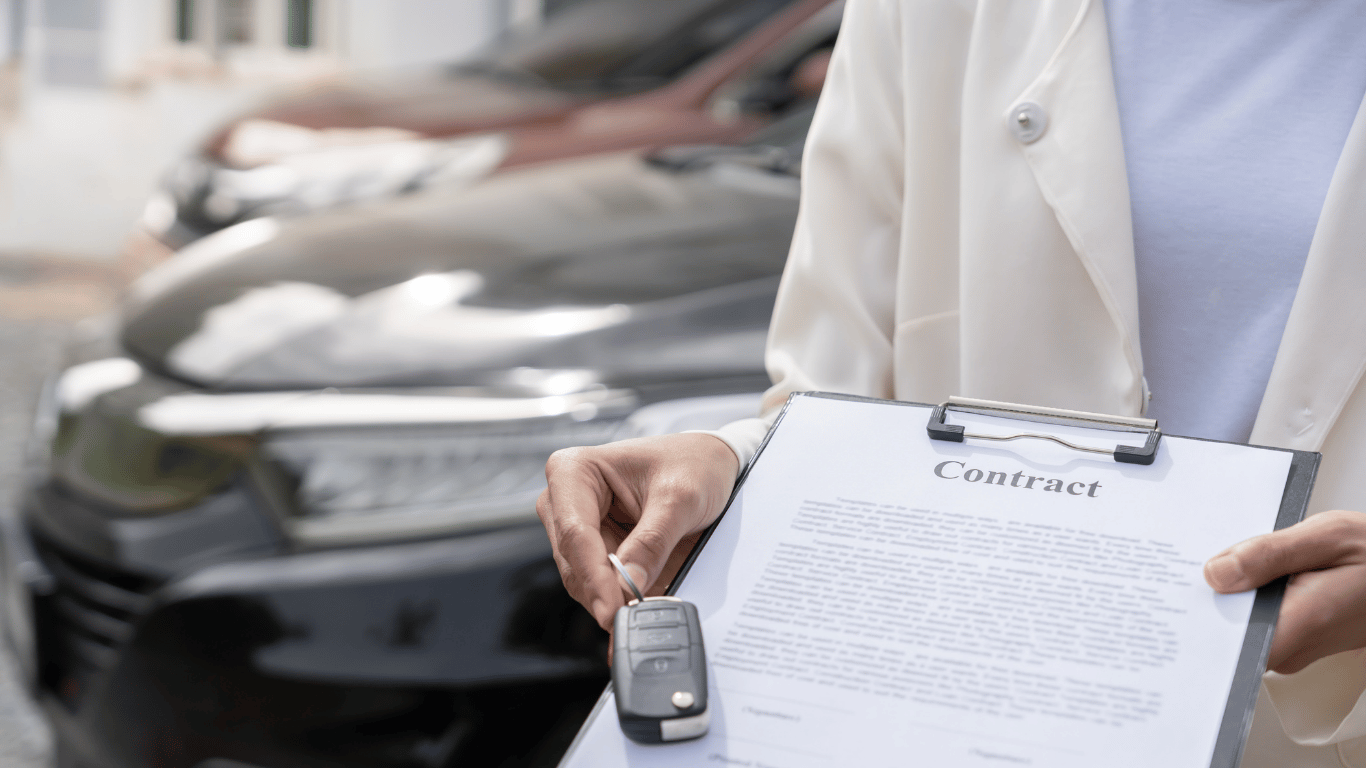

Financing a car in Brazil can be a practical solution for those who don’t have the full amount available but want to make the dream of owning a vehicle come true.

The process involves a few simple steps that make this access quicker and easier. If you’re thinking about financing a car, understanding how this process works is essential to making the best choice.

Before making this decision, it’s important to know that the market offers various options, each with its own conditions and rates.

Banks like Bradesco and Santander offer car financing with varying terms and installment amounts, allowing you to find the best option for your financial profile.

Car Financing in Brazil: How It Works and Where to Start

Car financing is a type of credit offered by banks and financial institutions, where the customer pays the vehicle’s value in monthly installments, plus interest. This is one of the most accessible ways to acquire a new or used car.

When financing a car, the bank lends the vehicle’s value, and the customer commits to paying this amount with interest and fees within a predetermined period.

Unlike a consortium, financing allows immediate acquisition of the car, while in a consortium, you must wait for a draw. A personal loan does not require the asset to be pledged as collateral.

For example, a person who chooses to finance a car worth R$ 50,000 can spread this amount over up to 60 installments, with an interest rate varying according to the chosen bank.

How the Car Financing Process Works

The car financing process starts with choosing the vehicle. After deciding on the model, the next step is to simulate the installment amount.

Then, the bank or financial institution performs a credit analysis to check the buyer’s financial history and determine the payment conditions, such as interest rates and terms.

Once approved, the contract is signed, and the customer receives the car. From there, they begin paying the agreed installments to the financial institution.

Simulating the financing on platforms from institutions like Bradesco or Itaú is essential to know the exact amount of the installments before closing the deal.

What Are the Common Conditions for Car Financing?

Financing conditions can vary according to the bank, but they generally include the interest rate, down payment, and the number of installments.

The most common terms are 24, 36, 48, or 60 months, and the interest rate can be fixed depending on your financial profile and the bank chosen, such as Bradesco or Santander.

The down payment, which can be made in cash or with the trade-in vehicle, usually ranges from 20% to 30% of the car’s value.

In general, financing covers 80% to 90% of the car’s value, but the total amount financed will depend on the bank or financial institution’s evaluation.

What Documents Are Needed to Finance a Car?

To start the financing process, you will need to present some essential documents, such as:

- CPF (Brazilian tax ID);

- RG (identity card);

- Proof of address;

- Proof of income.

Each bank may require additional documents, but these are the most common for those seeking vehicle financing, like Santander’s car financing or Banco do Brasil.

If your name is cleared on your CPF, the chances of approval increase significantly. Having bad credit can make the process more difficult.

Additionally, documents such as a marriage or birth certificate may be required, depending on the financial institution’s requirements.

How to Calculate the Installment Value in Car Financing?

To calculate the installment value in car financing, you need to consider:

- The vehicle’s value;

- The interest rate;

- The number of installments.

Many financial institutions offer online simulators, like Bradesco’s car financing, which allow you to see the impact of interest on the installments before closing the contract.

If you have a larger down payment, the financed amount will be lower, which can significantly reduce the installment amount.

Using a simulator can help plan the payment better, adjusting the installment value to your budget.

How to Simulate Car Financing?

Simulating car financing is easy and can be done directly on the banks’ websites, such as Bradesco’s car financing or Santander’s.

The simulation allows you to see the interest rates, the number of installments, and the required down payment to finance the car.

It’s important to compare the conditions offered by different banks before deciding which institution offers the best option for your profile.

When financing a car, it’s essential to perform simulations to ensure the conditions match your payment capacity.

What Are the Advantages of Financing a Car?

The main advantages of financing a car are:

- The ability to acquire a new or used vehicle without needing the full amount upfront.

- The possibility of choosing the terms, making the monthly installments more accessible, as is the case with Banco do Brasil.

- The opportunity to have a new model, with a factory warranty and a lower likelihood of mechanical issues in the first few years.

- The ability to secure lower interest rates, especially for those with a good credit history. This makes it even easier to pay off the financing.

What Are the Disadvantages of Financing a Car?

While financing a car offers several advantages, it’s important to also know the disadvantages. Here are some points to consider:

- The interest rate can be high, especially for those with a not-so-positive credit history. This can significantly increase the car’s total cost.

- The installment amount can take up a considerable part of your monthly income, limiting other expenses or investments you might want to make.

- Financing can extend over several years, meaning you’ll be committed to paying for the car for a long period, affecting your budget over time.

- If you cannot meet the installment payments, the vehicle may be repossessed by the financial institution, resulting in the loss of the asset and a negative impact on your credit history.

In the end, the total amount paid for a financed car can be much higher than the cash price, due to interest and other involved fees.

First Car Purchase: How Does Financing from Scratch Work?

When you decide to finance your first car, it’s important to understand the entire process and what to expect along the way.

The first car purchase may seem challenging, but with financing, this dream becomes more accessible.

What to Consider Before Financing Your First Car

Before financing your first car, it is essential to analyze your budget and decide how much you can commit monthly to the installments.

If possible, offering a down payment can reduce the financed amount and lower the installments.

Banks like Bradesco and Santander offer lower interest rates for those with a good financial history, which can ease the process.

How the Financing Process from Scratch Works

The process starts with choosing the car and simulating the installments. Banks like Itaú and Caixa Econômica allow you to see the installment amount based on the chosen model.

After the simulation, the bank does a credit analysis. For those with no down payment, the full car value will be financed, but this may result in higher installments and interest rates.

What Are the Common Conditions for First-Time Car Buyers?

Financing conditions usually include an interest rate that varies depending on your financial profile.

Bradesco and Santander offer terms between 24 to 60 months, with the option to pay a down payment or finance the full amount.

The down payment can be in cash or with the trade-in vehicle. If you don’t have a down payment, the bank can finance more of the car’s value, but this will impact the financing conditions.

How to Trade in Your Old Car for a Down Payment?

If you’re thinking of trading in your old vehicle at Santander, using it as a down payment is a great way to reduce the financed amount.

When the car is paid off, its market value is subtracted from the debt, making it easier to pay the monthly installments.

If the car isn’t paid off, the bank subtracts the remaining debt from the vehicle’s value. In this case, you’ll need to cover the difference in cash.

BV Financeira facilitates this process by offering affordable rates for those who already have a paid-off car.

Bradesco also allows the use of an old car as a down payment, but it’s important to verify the outstanding debt.

What to Do When the Old Car Is Not Paid Off?

If you’re thinking about trading in your vehicle at Santander with debt, know that it’s possible to use the car as a down payment even with the remaining debt. This helps reduce the financed amount.

When the car is still financed, the bank will evaluate the vehicle’s value and subtract the debt from the down payment. The difference needs to be paid by the customer.

When financing a car in such a situation, the installments may be higher, as the full value of the new car will be greater. However, this allows you to acquire a new model.

Santander offers solutions for those who want to trade in a car with debt, such as additional loans to cover the difference, making approval easier.

When the Debt on the Old Car Is Higher Than the Market Value?

If you’re thinking of trading in your vehicle at Santander with debt, know that when the car’s debt exceeds its market value, you will have to pay the difference.

A negative debt balance occurs when the car’s debt is higher than its market value. This can complicate the trade-in process.

To finance a car in this situation, negotiation is required. Itaú offers solutions, such as extra installments, to cover the difference.

You can also opt for financing a car with negative debt BV, where the financial institution helps negotiate the negative balance, allowing you to trade in the vehicle.

How to Compare Interest Rates from Different Financial Institutions?

Comparing interest rates for car financing at Caixa is essential for those looking for the best conditions. A difference of a few percentage points can significantly impact the total amount paid on the financing.

When financing a car, interest rates vary between institutions. This means that one bank may offer better conditions depending on your financial profile.

For example, comparing Bradesco financing interest rates with Caixa Econômica Federal’s shows that each offers terms and rates that cater to different credit profiles and needs.

That’s why it’s always a good idea to research and simulate different banks to see which institution offers the best financing deal for your budget.

What Are the Alternatives to Traditional Car Financing?

If you don’t want or can’t finance a car, there are other options in the market that can be interesting, like consortia and personal loans.

- Car Consortium: A consortium is an option for those who don’t need the car immediately. It allows you to parcel the value without interest, only with administration fees.

- Personal Loan: A personal loan can be an option for those who need immediate money and want to buy a car without the bureaucracy of traditional financing.

- Car Leasing: Leasing allows the use of the car with the option to buy it at the end of the contract. It’s ideal for those who want to test the vehicle for a while without long-term commitment.

- Car Sharing: A modern alternative is car sharing, where you pay for use without ownership commitment. Ideal for those who don’t use the car daily.

Santander Vehicle Consortium is a great choice for those who want to parcel without worrying about high interest, being an accessible option for patient buyers.

Personal loan for a car from Banco do Brasil is an alternative for those with a good relationship with the bank and looking for competitive rates.

These alternatives to traditional financing offer different ways to acquire a car, catering to each buyer’s profile and needs.

Conclusion

To sum up, throughout this article, you learned about different options for financing a car in Brazil, from traditional financing to alternatives like consortia and personal loans.

Each option has its advantages and disadvantages, depending on your financial profile and urgency in acquiring the vehicle. Always consider the best alternative for your budget.

Simulating financing with different banks and financial institutions is crucial to ensure you make the right decision. Don’t forget to check conditions and compare rates.

Liked the options? Want to discover which are the best institutions to finance a car in Brazil? Access the article below and learn everything about how to choose the best institution for your financing.

Best Institutions for Financing a Car in Brazil

Want to find out where to find the best financing conditions?

Trending Topics

Seasonal work in Australia: the perfect combination of income, opportunities and learning!

Discover how seasonal work in Australia can open doors to unique experiences, solid earnings and unforgettable opportunities.

Keep Reading

Amazon is Hiring: Find Your Career Opportunity

Are you looking for an exciting career? Amazon is hiring for various positions. Find the perfect job for you and join the digital revolution.

Keep Reading

Available Jobs at Walmart: How to Secure Your Position in the Company

Explore the available positions at Walmart and discover how to start a career full of opportunities and exceptional benefits.

Keep ReadingYou may also like

Remote work: the path to balancing work, free time, and quality of life!

Discover how remote work can transform your routine and open doors to incredible opportunities without leaving home.

Keep Reading

Free Electrician Course: Earn Up to $100,000 Per Year

Become a certified electrician and expand your professional opportunities. 100% online, free, and internationally recognized. Enroll now!

Keep Reading

FedEx Jobs: Opportunities for Growth and Development

Be part of a company that connects people and possibilities worldwide with FedEx jobs! Access our article now and find out what they are.

Keep Reading